Inside a City Carbon Market

August 21, 2017 | China, Climate Innovation Laboratory Cities, Consumption Reduction, Energy Efficiency

August 21, 2017 | China, Climate Innovation Laboratory Cities, Consumption Reduction, Energy Efficiencyby

SHANGHAI – The price of a ton of carbon emissions reached a high of 36 yuan, about US$6, the other day on this city’s unique trading exchange, which regulates more than 300 local enterprises, including the world’s busiest port, and the enormous Pudong airport. Shanghai’s four-year-old market is one of just a few city carbon markets in the world, set up as one of seven city pilots for the national market that China started to unroll this year. (Tokyo also has a local carbon market focused on commercial buildings.)

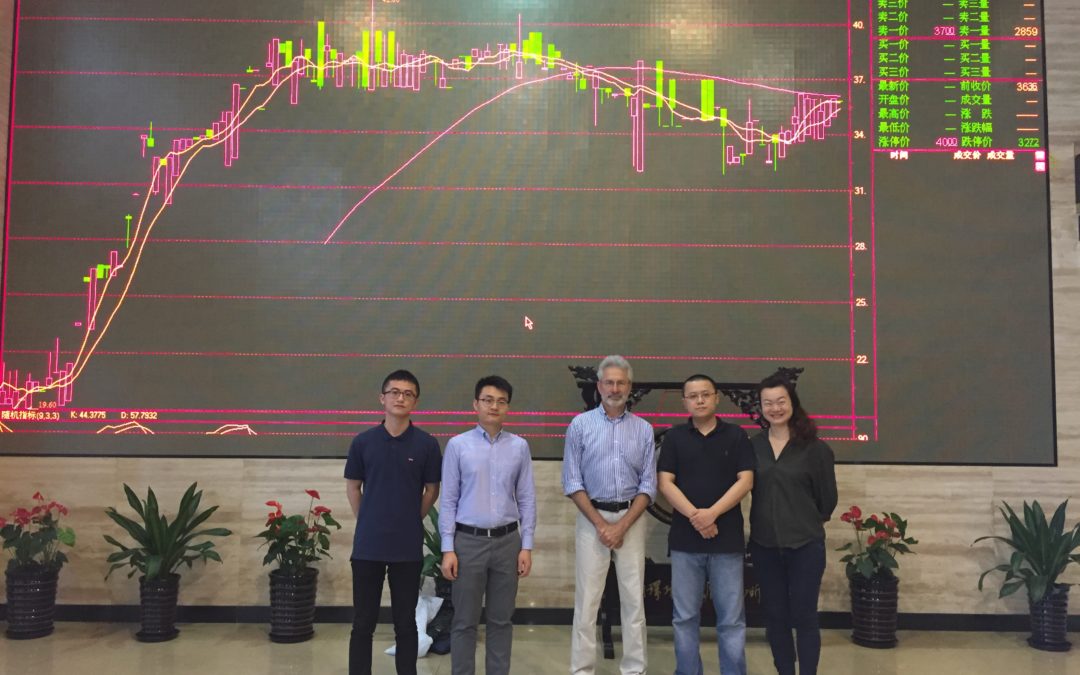

The city had to design the Shanghai Environment and Energy Exchange (SEEE) from scratch, looking at the experiences of the European Union’s market, which has had its ups and downs, and California’s trading market. It also had to figure out how to operate the market—which happens inside an unremarkable building on Shanghai’s North Zhongshan Road alongside one of the city’s elevated highways. In the quiet office I visited, as many as 60 employees work at computers or leave to visit with companies in the market. On one wall a gigantic computerized board displays trading prices. More real-time trading information is available through a transaction partner.

Since opening in late 2013, the market has expanded coverage to 310 companies in 26 sectors. More than 50 percent of Shanghai’s carbon emissions are included in the market, explains Guo Jianli, vice director of the Resource Conservation and Environmental Protection Division of the Shanghai Development and Reform Commission. The city's industrial sectors account for more than a third of its GDP, and its population has been growing. Through July 2017, Exchange officials report, some 26.8 million tons of carbon-emissions allowances (SHEAs) have been traded at a total cost of more than 400 million yuan (about US$70 million). After a three-year start-up period, the market required companies to obtain emissions allowances annually, most of which is done in the first half of the year. The enterprises report on the previous year’s emissions, which are verified by a third party. The market has also been developing carbon-financing programs with several banks, a spot market for trading, and a forward or futures market.

A critical design element was a decision not to create a price floor or ceiling for the market, says Zang Ao Quan, supervisor of the Exchange’s Trading Department. At one point the trading price went down to 5 yuan, about three-quarters of a US$1. Compared to other carbon markets, the Shanghai price has been relatively low. [California’s price, for instance, has averaged between US$12-14 per ton during the past three years. The price in the European Union market has hovered around US$6 for the past 18 months.] And this of course can diminish the financial motivation of companies in the market to reduce energy consumption and carbon emissions to avoid having to purchase allowances. The overall level of emissions in the market is set by national policy, which aims to peak carbon emissions nationally in 2030, a less aggressive stance than government entities that have established other carbon markets. Shanghai and dozens of other Chinese cities have committed to reach their carbon emissions peak before then. In Shanghai’s case, the goal is to peak by 2025. For the short-term, constraining the growth of energy consumption is the focus of city efforts.

For several years it has appeared that the Shanghai market might continue to operate in parallel with the national carbon market that China decided to establish. The national market launched in 2017 only covers a few industrial sectors. Considering the complexity and difficulty of establishing a carbon trading market, it seems likely that it will take several years to expand the national market substantially--and that city-based markets will stay in business.